Regulatory uncertainty surrounding stablecoins could place traditional financial institutions at a greater disadvantage than cryptocurrency companies, according to Colin Butler, executive vice president of capital markets at Mega Matrix. This sentiment highlights a growing tension between the established financial system and the rapidly evolving digital asset landscape, with potential implications for market stability and innovation.

The Dilemma for Traditional Banks: Investment Without Deployment

Butler articulated that major financial institutions have already made significant investments in digital asset infrastructure, including blockchain technology and digital asset custody solutions. However, these investments remain largely underutilized due to the ongoing legislative debate regarding the classification of stablecoins. "Their general counsels are telling their boards that you cannot justify the capital expenditure until you know whether stablecoins will be treated as deposits, securities, or a distinct payment instrument," Butler explained to Cointelegraph. This legal ambiguity creates a significant bottleneck, preventing banks from fully leveraging their technological advancements and exploring new revenue streams within the digital asset space.

Several prominent banks have indeed been at the forefront of developing the necessary infrastructure. JPMorgan, for instance, has developed its Onyx blockchain payments network, a significant step towards integrating blockchain technology into its existing payment systems. BNY Mellon has launched digital asset custody services, signaling its readiness to handle and secure a range of digital assets, including tokenized securities and stablecoins. Citigroup has also been actively experimenting, notably testing tokenized deposits, which could represent a future iteration of how banking services are delivered.

The substantial capital expenditure involved in building this infrastructure is undeniable. However, the inability to fully deploy these technologies due to regulatory ambiguity effectively caps the scalability of these investments. Risk and compliance departments within these institutions are understandably hesitant to approve full-scale deployment without a clear understanding of the legal and regulatory framework governing stablecoins. This cautious approach, while prudent from a risk management perspective, inadvertently places these institutions in a less agile position compared to their crypto-native counterparts.

The Crypto Advantage: Agility in Regulatory Gray Areas

In contrast, cryptocurrency firms have historically operated within a more fluid regulatory environment, often navigating "gray zones" for extended periods. This experience has fostered a degree of adaptability and resilience. Butler observed that crypto firms are likely to continue operating in these less defined spaces, a capability that traditional banks, bound by stringent compliance and regulatory oversight, cannot easily replicate. "Banks, by contrast, cannot operate comfortably in that gray area," he stated. This fundamental difference in operational flexibility suggests that crypto companies may be better positioned to innovate and capture market share in the interim, while traditional banks remain in a state of cautious observation.

The Widening Yield Gap: A Catalyst for Deposit Migration

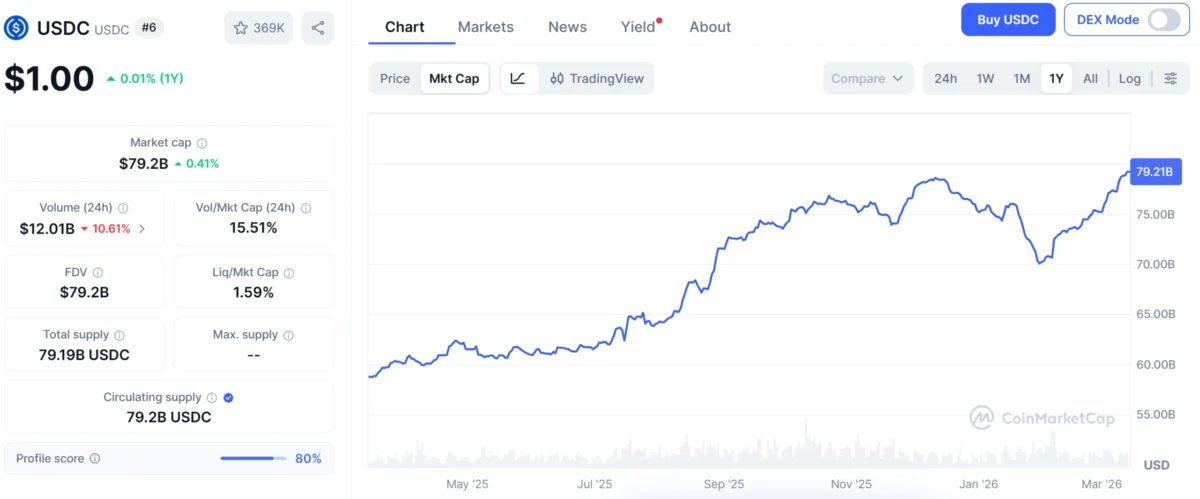

Beyond the regulatory hurdles, a significant economic factor is contributing to the potential displacement of traditional banking services: the widening yield gap between stablecoin platforms and conventional bank accounts. Butler pointed out that cryptocurrency exchanges often offer attractive annual percentage yields (APYs) ranging from 4% to 5% on stablecoin balances. This stands in stark contrast to the average U.S. savings account, which currently yields less than 0.5%.

Historical precedent suggests that depositors are highly responsive to yield differentials. Butler drew a parallel to the 1970s, when a significant shift of funds occurred from traditional bank accounts into money market funds, driven by higher yields. The current situation, he argued, has the potential to accelerate this migration even further. The ease of transferring funds from traditional bank accounts to stablecoin platforms, often taking mere minutes, coupled with the substantial yield disparity, creates a compelling incentive for individuals and businesses to seek higher returns in the digital asset space.

Fabian Dori, Chief Investment Officer at Sygnum, acknowledged the growing competitive gap but cautioned against an immediate, large-scale exodus of deposits. He emphasized that while the yield differential is meaningful, institutions still prioritize trust, regulatory clarity, and operational resilience when managing their liquidity. These factors, he suggested, might act as a moderating force in the short term.

However, Dori also recognized the potential for accelerated migration at the margins. "The asymmetry can accelerate migration at the margin, especially among corporates, fintech users, and globally active clients already comfortable moving liquidity across platforms," he noted. This suggests that sophisticated market participants, who are less risk-averse and more attuned to yield opportunities, could be among the first to shift substantial assets. The critical inflection point, according to Dori, will arrive when stablecoins are unequivocally recognized and regulated as "productive digital cash" rather than mere "crypto trading tools." At that juncture, the competitive pressure on traditional bank deposits will become significantly more pronounced.

The Risk of Offshore Capital Flight: Unintended Consequences of Regulation

Butler also raised a critical concern regarding the potential unintended consequences of regulatory interventions aimed at curbing stablecoin yields. He warned that attempts to restrict stablecoin yields could inadvertently push capital into less regulated and potentially riskier offshore markets. Under current U.S. law, stablecoin issuers are generally prohibited from directly paying yield to holders. However, cryptocurrency exchanges have found ways to offer returns through various mechanisms, including lending programs, staking, and promotional rewards.

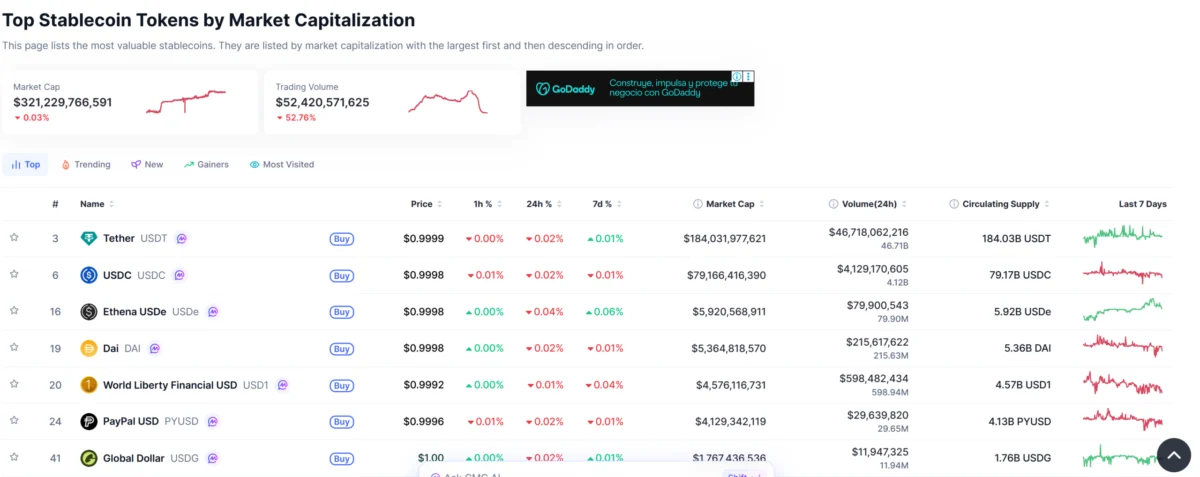

If lawmakers impose broader restrictions on these yield-generating activities within regulated stablecoin frameworks, capital seeking returns is likely to seek alternative avenues. One such avenue is the growing market for synthetic dollar tokens. Products like Ethena’s USDe, for example, generate yield through strategies involving derivatives markets rather than relying on traditional fiat reserves. These mechanisms can offer competitive returns even when regulated stablecoins face limitations.

The acceleration of this trend could lead to a paradoxical outcome: instead of enhancing financial stability, regulatory restrictions might drive capital towards opaque offshore structures with significantly fewer consumer protections. "Capital doesn’t stop seeking returns," Butler emphasized. This highlights a fundamental challenge for regulators: balancing the need for consumer protection and financial stability with the inherent global and fluid nature of capital flows in the digital age. The pursuit of yield is a powerful economic force, and attempts to dam it in one location may simply cause it to overflow into less visible and more unpredictable channels.

Broader Implications and Future Outlook

The regulatory uncertainty surrounding stablecoins and the resulting dynamic between traditional banks and crypto firms have far-reaching implications. For traditional banks, it represents a critical juncture where their legacy infrastructure and regulatory compliance requirements could hinder their ability to compete in a rapidly evolving financial landscape. Failure to adapt could lead to a gradual erosion of market share, particularly in areas related to payments and savings.

For the broader financial ecosystem, the situation underscores the need for clear and comprehensive regulatory frameworks that can foster innovation while mitigating systemic risks. The debate over stablecoin classification is not merely a technicality; it is central to determining the future role of digital assets in the global economy. A well-defined regulatory approach could unlock significant opportunities for banks to integrate digital assets into their offerings, potentially leading to more efficient and accessible financial services for consumers and businesses alike.

Conversely, continued regulatory ambiguity risks fragmenting the market, driving innovation into less transparent corners of the digital asset space, and potentially exacerbating financial risks. The potential for capital to flow offshore in search of yield, as warned by Butler, is a tangible concern that regulators must address proactively.

The development of technologies like blockchain and the emergence of stablecoins represent a fundamental shift in how financial transactions can be conducted. Traditional financial institutions, with their established infrastructure and client base, are uniquely positioned to bridge the gap between the traditional and digital financial worlds. However, their ability to do so hinges on regulatory clarity. Without it, the competitive advantage may continue to lie with agile crypto firms, and the potential benefits of these innovations may be realized by a segment of the market that operates outside the purview of established financial oversight. The coming months and years will be crucial in shaping the regulatory landscape and determining whether traditional banks can effectively navigate this new frontier or if they will cede ground to a more dynamic and less regulated digital asset sector. The "yield gap" serves as a stark reminder that in the world of finance, capital is always in pursuit of the most attractive returns, and regulatory frameworks must evolve to accommodate this reality while safeguarding financial stability.